Types of HECM Reverse Loans

There are several loan options in the HECM program designed for your goal or need.

There are several ways to structure a HECM reverse mortgage depending on your financial goals, lifestyle needs, and retirement plan.

Some homeowners use a HECM to create flexible access to cash over time, while others use it to eliminate monthly mortgage payments or support long-term retirement planning.

.jpg)

HECM Line of Credit

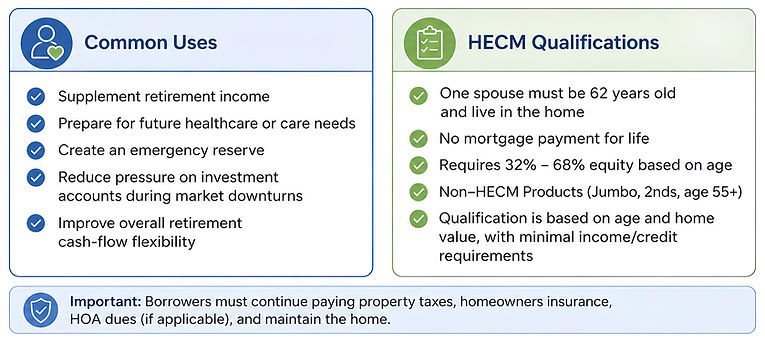

A HECM Line of Credit allows eligible homeowners age 62+ to convert a portion of their home equity into accessible funds while continuing to live in their home.

Unlike a traditional home equity line of credit (HELOC), the HECM Line of Credit is specifically designed for older homeowners and does not require mandatory monthly mortgage payments as long as loan obligations are met.

%20(1).jpg)

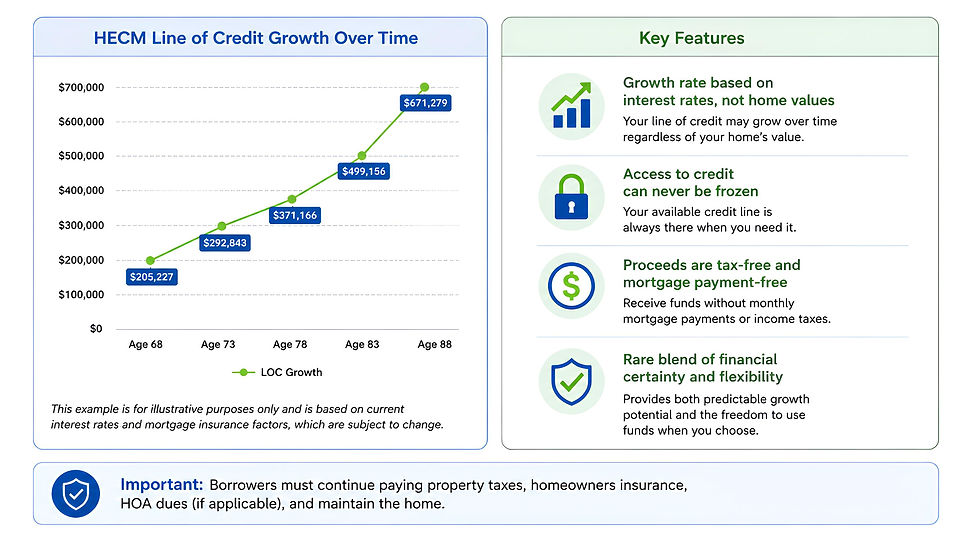

HECM Line of Credit Growth Rate

How it Works

One unique feature of the HECM Line of Credit is that the unused portion of the available credit line may grow over time. This growth is not tied to home appreciation, but instead is based on the loan’s interest rate and mortgage insurance factors.

.jpg)

Because of its structure, many financial planners view the HECM Line of Credit as a valuable tool for supporting retirement planning flexibility.

HECM Lump or Partial Sum Payout

A HECM reverse mortgage can provide homeowners with access to a lump sum or partial payout from their available home equity. This option is often used to pay off an existing mortgage, cover large expenses, complete home modifications, or create additional retirement cash-flow flexibility.

Unlike traditional loans, repayment is deferred while the borrower continues living in the home and meets loan obligations such as property taxes, insurance, and home maintenance.

Additional Types of HECM Reverse Loans

In addition to traditional HECM reverse mortgages, some homeowners may benefit from specialized proprietary reverse mortgage solutions. These options are designed to provide greater flexibility for higher-value homes or unique financial situations that may fall outside standard HECM guidelines.

Whether you are looking to access additional equity, maintain a low existing mortgage rate, or explore larger borrowing opportunities, these alternative reverse mortgage products may help support your retirement goals and long-term financial strategy.

.jpg)

Explore Which HECM Reverse Mortgage

Best Fits Your Retirement Strategy

Every homeowner’s retirement goals and financial situation are different. A HECM reverse mortgage is not a one-size-fits-all solution, which is why understanding your options begins with education and thoughtful planning.

Whether you are looking to improve monthly cash flow, eliminate mortgage payments, create a flexible Line of Credit, prepare for future healthcare needs, or support long-term retirement planning, there may be a HECM strategy designed to fit your goals.

At Live Better Financial, our experienced mortgage advisors help homeowners explore how home equity strategies — including HECM reverse mortgages — may provide additional flexibility and confidence in retirement.

Schedule a free consultation to learn more about your options and determine whether a reverse mortgage is a good fit for your situation.

Have questions about HECM loan program options? Call (888) 225-3336 or schedule a consultation.